Don't Fight the FANG!

Why the internet giants keep growing at insane rates and why their already huge competitive advantages will keep accelerating over time.

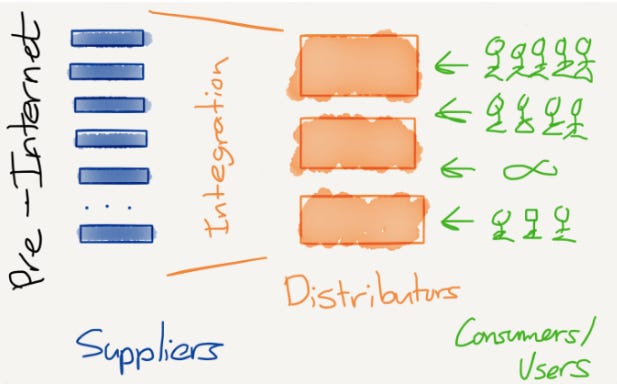

The value chain in a marketplace is driven by three parties: the supplier, the distributor and the consumer. To achieve outsized profits companies either want to monopolise one party or integrate two or more parties and gain a competitive advantage.

The technology/strategy analyst Ben Thompson has an outstanding framework to understand internet companies: Aggregation Theory. It explains how companies use the internet to reform value chains, increase their influence and maximise their profits.

The Pre-internet Era

Prior to the internet, distribution was the bottle neck in the value chain. If you wanted to write a book/paper/movie etc., there was always the problem regarding how to print and distribute it. You had to turn to someone who had invested in printing equipment and distribution network to actually get your product in front of an audience. Because of this it was rational to integrate supplier with distributor to optimise the process.

This meant that the supplier/distributor could reach hundreds, thousands even millions of consumers, but consumers were stuck with whatever content (newspaper, TV, radio) the supplier/distributor decided would sell. Individualising content was not feasible because of the high costs that would be incurred. Not only were consumers limited by what suppliers/distributors think would sell, but also by geography and shelf space.

The Post-internet Era

Internet totally changed the value chain dynamic. No longer was distribution the limiting factor in a value chain. Internet could now offer you exactly what you wanted, when you wanted.

With the internet the marginal cost of reaching consumers went to 0 (or close to 0), which meant that the bottleneck in the value chain was transferred from distribution to consumer. There is only 24 hours per day after all and the challenge became winning over the end users limited time and attention.

Aggregators - The Ultimate Platform

This is where aggregators come into the picture. Aggregators are platforms with a direct relationship to the end user and as such own the consumers attention. This is why it is called aggregation theory: They aggregate the consumers needs in one destination.

Aggregators have 0 (or close to 0) marginal costs for new customers. Traditional companies have to endure up to 3 different costs to serve new customers:

Cost of goods sold - the cost of producing a product or service to the consumer

Distribution costs - the cost of getting that product or service to the consumer

Transaction costs - the cost of getting paid for your product or service

Aggregators simply do not incur these costs: Digital goods have a 0 marginal cost to sell (although they do have a fixed cost), they are delivered over internet and thus have 0 distribution costs, and transactions are automatic which make the transaction costs go to 0. Obviously there might be certain costs that occur in certain circumstances, like increased server costs for more users or credit card fees, but as a whole they are negligible.

This means that Amazon’s traditional retail operation or Apple’s hardware division are not pure aggregators. On the other hand, Apple's app store and Amazon Merchant Services are. This doesn’t mean that Amazon or Apple’s platforms are bad, just that they do not enjoy all the upsides of a pure aggregator. Not to mention that Amazon can leverage their size for distribution costs, so even if their retail operation is not an aggregator they still have a large moat in retail.

Since aggregators facilitate the interaction between two or more parties in the value chain (such as supplier and consumer), suppliers will join the aggregator to sell their goods which over time results in an abundance of supply on the aggregators platform. This results in superior discovery of products/services for the end users which will attract even more users because of the great experience.

When more consumers use an aggregator, more suppliers will join (effectively commoditising themselves) to sell their goods, which will make the platform even better, which will attract more consumers, which will attract more suppliers in a virtuous cycle.

This means that the acquisition cost of customers decrease drastically over time for aggregators. It’s network effect deluxe.

Google is a great example of this: Their excellent search functionality attracted an initial user base which over time became a large user base when other consumers realised that Google’s search was better than competitors.

Since consumers (the users) preferred using Google, the suppliers (companies) wanted to be seen on Google and started to adapt their websites to rank higher in the search results. This made Google’s search function even more effective which gave consumers an even better user experience which in turn made more suppliers willing to adapt their websites for Google’s search.

For Google this resulted in a network effect and moat which is almost impenetrable. It also gave rise to a whole new industry: Search Engine Optimisation, optimising a website or ad to rank higher with the Google search algorithm.

Aggregators as such have a strong winner-take-most or winner-take-all effect since aggregator platforms become better for each additional user and winning over consumers as an incumbent/competitor becomes increasingly more difficult.

This should be compared with non-aggregators/platforms where customer acquisition costs increase with scale. This is because initial customers have a perfect “product-market fit”, but when the product scales the product-market fit gradually decreases and the product’s value becomes lower for new customers.

Generally this applies to companies that produce products/services in-house. This is because there is a natural limit for how many customers can be attracted to one or a couple of products.

This is one of the reasons why Disney+ should not be considered a direct competitor to Netflix (or a “Netflix Killer”). Yes, they both produce movies, but they have widely different business models. Disney+ is part of a larger ecosystem to sell products and Netflix is an aggregator providing consumer attention to suppliers.

Super Aggregators

An aggregator owns the relationship to the end user and has the ability to scale this relationship, but there are several levels of aggregators depending on their relationship with suppliers.

Level 1 Aggregators: Supply Acquisition

This level applies to companies like Netflix who have to pay to get supply (content) to their platform. Content is a fixed cost that provides value for all future Netflix customers. More content equals more customers since the value of the platform increases. Increased value results in more users with longer engagement time.

The more customers Netflix has, the more they can spend on new content. For every additional unit of content Netflix produces or adds to their platform, they lower the customer acquisition cost for future customers.

This is comparable with traditional software companies cost structure and revenue models. Users and revenues increase exponentially with time while costs are fixed. When unit economics look like this it’s possible to create an extremely profitable company if the user base is scaled to critical mass.

What happens when the marginal cost is not 0? One example is Spotify’s current music division where Spotify has to pay royalties for each song that is streamed on their platform. This means that the more their music platform is used, the more they have to pay. This does not result in the leverage that aggregators experience.

With that said, it is most likely that this will change over time for Spotify with increased leverage over record labels and monetisation of other divisions like podcasts.

Level 2 Aggregators - Supply Transaction Costs

These aggregators do not own their supply, but rather pay suppliers to bring them on their platform. Airbnb is an example of a level 2 aggregator. Real estate is not owned by Airbnb, but is provided by a third party. This incurs costs in the form of background checks, verification and regulation.

Level 3 Aggregators - Zero Supply Costs

These companies do not own their supply and do not incur supply transaction costs. Social media companies (Snapchat, Twitter) is an example of this where supply (in the form of content) is made by initial users which attracts more users that produce more content and so on.

Level 4 - The Super Aggregators

These companies have a three party market place - users, suppliers and advertisers - where no party has any marginal costs. Facebook and Google are typical super aggregators.

They attract users and suppliers at no cost and can scale perfectly, and have a “self serve” ad platform that generates revenue with no variable costs. This makes them extremely efficient at scaling supply, demand AND revenues.

Because aggregators become better for each additional user it is reasonable to assume that growing aggregators will keep growing since more users will be attracted to them. This is one of the main reasons why these companies receive a premium valuation in the markets.

This doesn’t guarantee that an investment in an aggregator will result in outsized returns or even be a good investment, but the probability that a growing aggregator will keep growing moving forward is undoubtedly high.

Did you enjoy this newsletter? Please subscribe if you haven’t already!

Original tweet from 02 August 2020: